Four months into this newsletter, it’s time for a telecom-ish post. Bring on the catchy acronyms!

The immediate catalyst - two announcements from Verizon related to 5G deployment; a second catalyst: I am starting to get newsletters about 6G. Yes, 6G! Which looks to be even more challenging than 5G to deploy. More on that in a moment.

First, the news from Verizon:

In its 2022q2 earnings, Verizon announced 47% of its postpaid subscribers were on 5G phones. This is up from 34% as of their 2021q4 earnings. Put another way, Verizon sold ~12M 5G phones to postpaid subs over that time, or about 2M 5G handsets per month. Slow and steady wins the race? Some back-of-the-envelope calculations are below:

And yes, the headline there is that retail postpaid subscribers are FLAT.

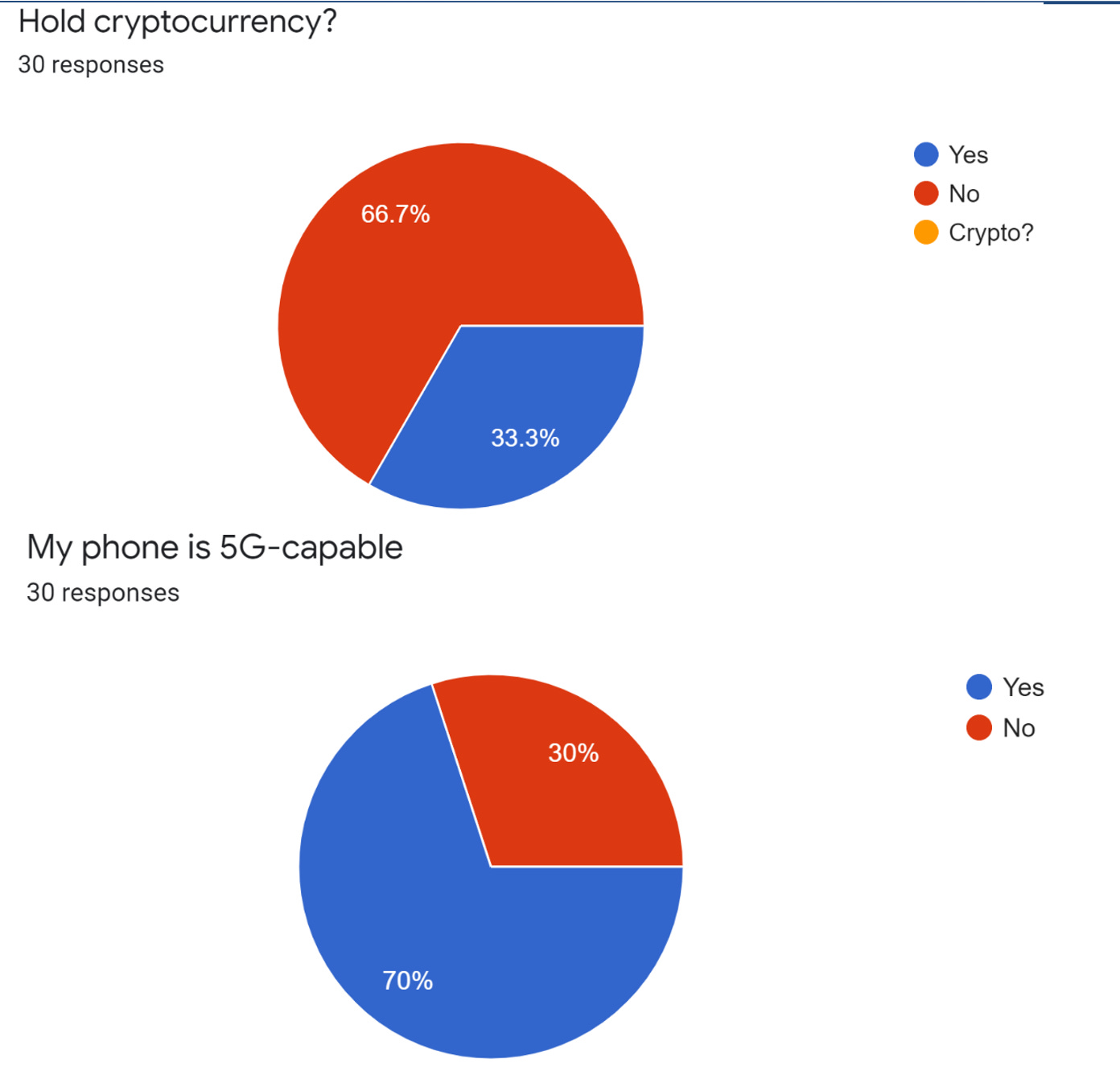

Note that new generations of technology are adopted in a distribution. In a poll this January, prior to spring 2022 Strategy for the Networked Economy class, 70% of respondents had 5G-capable phones (n=30, January 2022). (And, for what it’s worth, 34% held crypto.) So earlier adopters (of, say, the iPhone 12 and above), already had 5G phones.

MBA class poll, January 2022. n=30

Announcement #2: perhaps not coincidentally, last week Verizon announced it was migrating customer traffic to 5G core.

Cellular networks can be divided into RAN and Core. RAN = Radio Access Network. Essentially, the cell sites you see along highways or on top of poles or hanging from the corners of buildings. Like this one in Mill Valley in Marin.

Quiet tenant provides steady rent income for the theater

Core refers to Enhanced Packet Core (EPC) or, to use a more traditional term, where the switching magic of network operation happens, at scale. GSMA, the global mobile operator association, provided the reference diagram below in 2019 for operators choosing how to roll out 5G. Incumbent operators who already had 4G (and below) networks generally chose the left option, semi-amusingly acronym’ed as NSA or Non Standalone.

GSMA reference diagram on 5G deployment options

This helps amortize existing investments and also acknowledges the reality that greenfield network operators (e.g. 5G-only) are few and far between. Reliance Jio and Rakuten, both of which started from 4G, are the unicorns that prove the rule. Generally, operators are managing multiple network generations in parallel, and existing subscribers need to be migrated over. For US subscribers, the handset refresh cycle is about once every three years. Apple waiting until the iPhone 12 to adopt 5G (remember, the first iPhone was 2.5G) was also a gating item.

In fall 2020, when I published Security Implications of 5G Networks with support from the UC-Berkeley Center for Long-Term Cybersecurity, one of my recommendations was that operators assess 5G core deployment as quickly as possible, for the security and functional benefits it would provide, such as the ability to “slice” networks and also more secure authentication between handset and base station. So VZ’s announcement of customer migration to 5G core implies these enhancements are now commercially available.

Coming on the heels of (finally) getting midband spectrum in January, which put the US big three operators on a relatively similar 5G spectrum footing, this feels like a tipping point for 5G service in the US.

It may, of course, be the case that these capabilities were already being made available to enterprise or government clients.

The five recommendations from my report back in fall 2020 are below:

Operators, their partners, and their customers investigate the viability of 5G-only service;

Operators and their partners develop the ability to rapidly deploy software updates, including security patches, to small cells, customer premise equipment, and other connected devices;

Operators and their partners develop the ability to rapidly test and verify devices from new partners from outside of the traditional telecom ecosystem;

Policymakers act to facilitate rapid deployment of 5G networks, including implementing policies to facilitate cell site acquisition;

Policymakers recognize the role of global standards bodies; of rapid standards development; and the economic value of globally harmonized standards.

On to 6G.

This spring, I was asked to help fill and moderate a panel on 6G. Ultimately we agreed it was a bit too early, which is a polite way of saying finding US speakers who had much to say on 6G was a struggle. (Here’s how Nokia describes 6G.) So it’s been interesting to see more newsletters about 6G and Thz wireless start show up in my inbox. Here’s a sample.

In my more techno-optimistic moments, 6G looks like what the metaverse could look like - wearable (and presumably rechargeable?) wireless, with daily attire as wireless-enabled motion suits. But, here on terra firma, network deployment tends to be gated by the difficult realities of site acquisition and operation, not to mention building compatible phones. More on this in a subsequent post.