Intel: Five generations and a culture change (Part 2)

Plus, semiconductor fabrication and the danger zone

Friends - very nice to hear some of you after my last post. Spring is springing here in NorCal - the blossoms are in bloom, even as the rain refuses to recede. California Water Watch with the update:

A warm welcome to new subscribers! Some of you are current or recent students; others came via

🙇♂️ . Thanks for being here! By way of introduction, in this newsletter I generally cover themes related to my instruction:Strategy for the Networked Economy

Clusters: Locations, Ecosystems and Opportunity

Business in Japan

Competitive Strategy

For those who came in via

- some, but not all, posts here will be on semiconductors, but this post will be! Open RAN is another topic I’ll be covering shortly.It was a pleasure to visit my faculty colleague Molly Turner’s Startup Regulatory Strategy Lab class to share some of my experiences doing federal business development, regulatory and congressional advocacy, and standards development back in the 2000s. I would have greatly benefited from access to such a class when I was student! Instead, like a lot of people in startup roles, I learned (a lot) by doing, with all the highs, lows and successes and avoidable mistakes that implies. So I am delighted Molly has put this class together to help students de-risk their regulatory strategies.

To set the stage, I shared some of the shortcomings of satellite navigation systems, such as those laid out in a Dept of Transportation Report in….2001. This is the well-known (and still unsolved) problem we were trying to solve. We picked terrestrial TV as our signal of opportunity in trying to solve this.

And while there were successes on the contracting front (DARPA contract!) and the standards front (ATSC Mobile DTV!), the company didn’t survive to reap the benefits of those successes. It was fun - and thought-provoking - to talk about this with a group of smart students. Thanks again to Molly for having me.

Last year, I wrote about how Intel, under Pat Gelsinger, had chosen the hardest tile on the board, by choosing to both accelerate through node generations faster than Intel ever had *and* simultaneously start a third-party services organization in the form of Intel Foundry. Either would be extremely hard on their own; Intel had chosen to do both. Here’s last year’s post.

Now, I got that headline wrong - it wasn’t four generations, it was five (5N4Y)! Here they are, in the now-familiar diagram.

But that just makes the hill steeper. For Intel has to run back up the hill to the technology frontier, while simultaneously going through a cultural shift, i.e., learning to be customer-friendly in providing foundry services to third parties. Further complicating this, some of the volumes that might help Intel’s foundry economics had to be to sent to TSMC, due to Intel’s repeated delays in getting to 10nm. As with last year’s post, I’m sharing a chart, originally from AnandTech, showing those delays. This is cited from the Intel Corporation: Outsourcing Dilemma (Ivey; 2022) case we use in class.

In their January 25, 2024 analyst call, Intel CEO Pat Gelsinger provided this update on 5N4Y:

Intel 18A is expected to achieve manufacturing readiness in second half '24, completing our 5 nodes and 4-year journey and bringing us back to process leadership. I am pleased to say that Clearwater Forest, our first Intel 18A part for servers has already gone into fab and Panther Lake for clients will be heading into fab shortly.

As we complete our goal of 5 nodes in 4 years, we are not satisfied nor are we finished. We have begun installation of the industry's first High-NA EUV tool in our most advanced technology development site in Oregon, aimed at addressing challenges beyond 18A. We remain focused on being good stewards of Moore's Law and ensuring a continuous node migration path over the next decade and beyond.

This is good news, on the technology front. On the demand side, challenges remain, whether in data center or client computing. (I will note the stock got hammered the next day, on soft guidance.)

But, why start Foundry, if racing back up to the technology frontier and redeveloping the tick-tock cadence of yesteryear will be hard enough? Is this a choice, or does Intel *need* Foundry as a business supporting third-party customers?

We discussed this as a class in Strategy for the Networked Economy, as fate would have it, the week before Intel Foundry Day.

Class is in two halves: in the first half, we discuss Qualcomm’s go-to-market as late-ish entrant trying to get network operator traction after the TDMA standard had been adopted. In the second half, we discuss the Intel outsourcing case. Thus, we have one of the most influential fabless semiconductor companies (Qualcomm), along with the company trying to implement IDM 2.0 (Intel).

One class theme is that of the innovation flywheel - R&D begets early success, which begets revenue, which enables more R&D, which enables subsequent growth, and more R&D. Qualcomm is a great example of this. Its success in merchant silicon led to Panasonic, Philips, Motorola and others ultimately exiting or spinning out their foundry businesses. They couldn’t match the combined scale of Qualcomm’s R&D; meanwhile, handset makers without captive semiconductor arms could benefit from Qualcomm’s aggregated demand and superior R&D.

Huawei is another. One driver behind the interest various governments have in Open RAN is fear that Nokia or Ericsson won’t be able to innovate enough on their own to keep up with Huawei.

Of course, this can break the other way. Companies can fall behind the cadence of the innovation cycle in their market, and face steep capital barriers to keep up.

In semiconductor fabrication, TSMC sets this cadence. With data from Capital IQ, I’ve graphed TSMC’s annual capex (in TWD, at about 31.5 NTD to USD) below. 2023 is a modest $30 billion.

TSMC capex

Here’s Intel’s, again, via Capital IQ.

Intel capex

To help us wrestle with this question, I invited

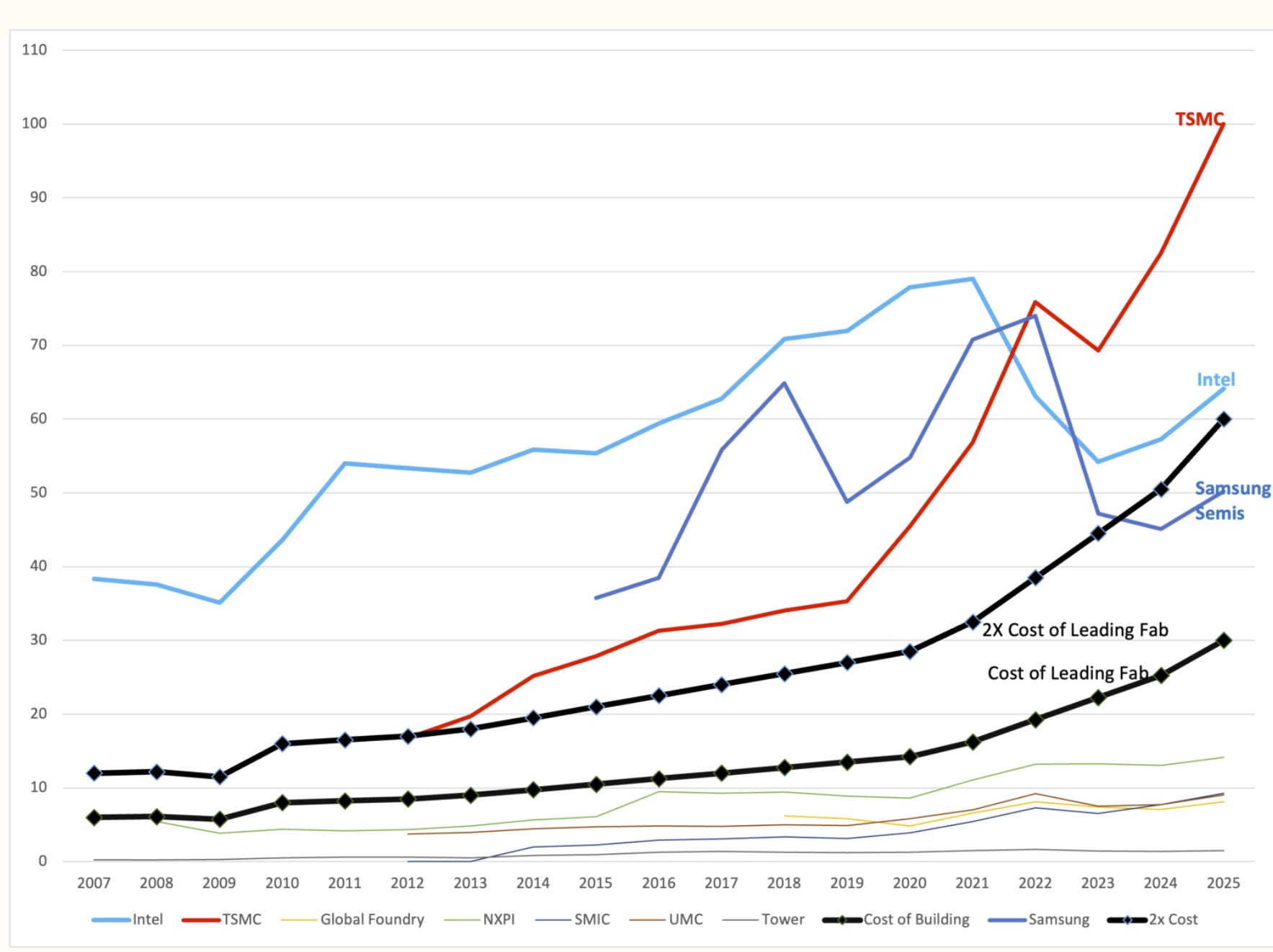

to join us. (Jay kindly joined us on mere days after came to campus!) Jay previewed analysis he would share in his newsletter on February 16 and on the Circuit podcast (Episode 55). This plots a rule of thumb - that to stay at the leading edge, fabricators need revenue at least 2x the cost of a leading edge fab. Jay noted that all fabs that had consistently dropped below that line had ultimately exited or given up on leading edge nodes (GloFo).

“danger zone” graph by Jay Goldberg,

This is originally posited (per Jay) by analyst Mark Lapacis in 2012; the question then was whether TSMC could afford to stay at the leading edge. Clearly, times have changed.

Here, the trend in Intel’s revenue is illuminating.

In particular, it highlights why Intel needs Foundry to work to stay at the leading edge - Intel needs third-party fabrication customer revenue to help feed its flywheel. For after 18A, will be 14A, and so on.

In this context, it was interesting that Secretary Raimondo joined Intel Foundry Day on February 21. Secretary Raimondo alluded to the need for a second Chips Act, at an event where some hoped she would announce specifics on funds to Intel from the 2022 CHIPS Act.

Applying this same rule of thumb, say, to the Rapidus project makes for an interesting calculation - can Rapidus get to, say, $40B/year in product revenue as a pure-play fab? I suspect Rapidus’ construction and staff costs will be lower than Intel’s. But for all that METI has done on the supply-side, there’s still the demand question, as Bloomberg highlighted recently.

Thanks again to

for joining us in class.The Economist and WSJ both had articles on the “San Francisco comeback”. Reading, I had two reactions.

The first evokes the famous Mark Twain quote - the rumors of San Francisco’s demise were greatly exaggerated.

That said, the comeback is a work-in-progress too. BART ridership, as of January 2024, was about 38% of January 2019. Hotel occupancy still lags. SFO enplanements (which would capture people who moved out the city) are closer to 2019 levels.

The second: I am glad AI is being made in the cool gray city of love (hat-tip: Gary Kamiya), for a lot of reasons. That said, as with Craiglist (born in the Sunset) or Google Search (born in the Peninsula), AI will likely have a lot of indirect employment impact, outside of the Bay Area where it is being nurtured.

Coming up - starting the week of March 11, I’ll meet two cohorts of first-year full-time MBAs in “Core” Strategy. Very much looking forward to meeting half of FTMBA 2025!

In honor of spring being in the air, here’s some Hugh Masekala.

Onward and upward!

Jon